On a vote of 55-0-0, the Consumer Fairness Act of 2019 (HB88) passed out of the Senate today with unanimous and bipartisan support. This legislation brings long-overdue relief to consumers who are trying to pay off their debts and achieve financial stability.

“The Consumer Fairness Act gives a fighting chance to thousands of Illinoisans who, up to this point, have been faced with the crippling reality of years of debt accumulation with a 9% interest rate,” said Kevin Herrera, staff attorney at the Sargent Shriver National Center on Poverty Law. “Critically, this new legislation also provides clarity around the debt collections process, letting people know what debts are being collected on ─and how long the collections process will last ─ sooner. We are thrilled that Illinois is on its way to joining several other states around the country in leveling the playing field between people who owe judgment debts and the collections industry.”

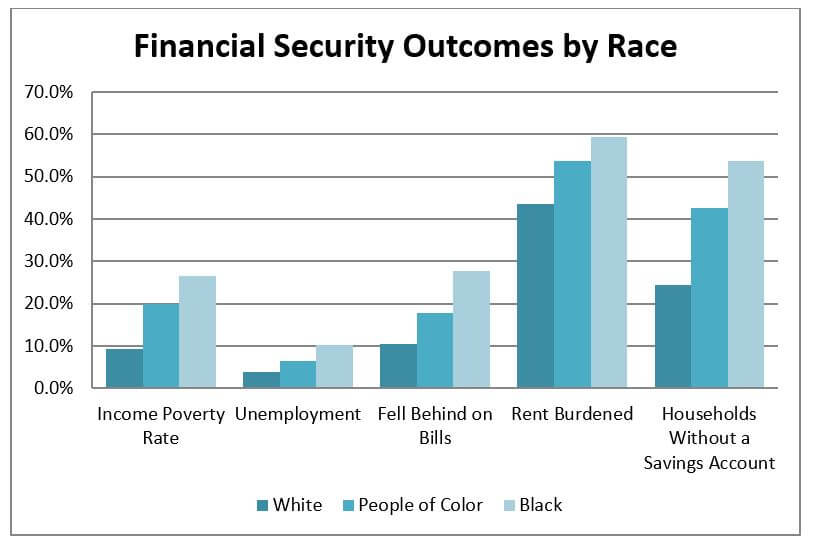

Nearly one in five Illinois consumers have debt that is in collections.[1] For decades, Illinois’ laws have made it difficult for families to pay their debts while also meeting their basic needs because the automatic interest rate on judgments is set so high, at 9%. As a result, Illinois has one of the highest bankruptcy rates in the country.[2]

Moreover, the burden of debt falls disproportionally on communities of color. In Illinois, predominantly nonwhite communities have twice as many individuals in collections as in predominantly white communities.[3]

“The racial wealth divide is massive in Illinois, with white households having 29 times more net worth than black households,” said Jody Blaylock, Project Manager for Financial Justice Policy at Heartland Alliance. “HB88 is an important step towards closing that divide by helping families get out of debt and build financial security.”

A coalition of legal aid and community organizations, along with Representative Will Guzzardi and Assistant Majority Leader Senator Iris Y. Martinez, led efforts to pass HB88 in the Illinois General Assembly to help consumers who are stuck in debt.

“With debt judgments collecting 9% interest for up to 26 years, debt is plaguing families across this state,” said lead bill sponsor Representative Will Guzzardi. “This legislation brings much-needed relief to Illinoisans who are trying to balance their budgets and get ahead.”

“The people of Illinois deserve the opportunity to get ahead,” said Assistant Majority Leader Senator Iris Y. Martinez, lead sponsor for the bill in the Senate. “I am proud to sponsor this legislation, which will help low-income families become financially stable.”

Under our current law, judgments accrue 9% interest for up to 26 years and the Consumer Fairness Act of 2019 is an important step towards giving all Illinoisans the opportunity to thrive by decreasing the post-judgment interest rate from 9% to 5%, and decreasing the timeframe to collect on a debt from 26 to 17 years. Taken together, these reforms will make debt more manageable and help families more quickly balance their budget and build financial security.

“Debt collection laws should reflect modern realities and treat everyone fairly,” said Ashlee Highland, Supervising Attorney at CARPLS. “The changes in HB88 will allow many of our clients to pay off their judgments rather than being saddled with financially debilitating wage garnishments, or filing for bankruptcy.”

A coalition of legal aid and community organizations urges the Governor to sign HB88 into law, ensuring that Illinoisans have a fair shot at paying their debt.

Check out the fact sheet for more information.

[1] Federal Reserve Bank of New York/Equifax Consumer Credit Panel, tabulated by the Federal Reserve Banks of Philadelphia and Minneapolis and accessed via the Consumer Credit Explorer (date accessed: May 2, 2019). Found at: https://www.philadelphiafed.org/eqfx/webstat/index.

[2] Prosperity Now Scorecard. 2019. Found at: https://scorecard.prosperitynow.org/data-by-location#state/il

[3] Illinois Debt Collection Fact Sheet. National Consumer Law Center. 2018.

Take Action!

Take Action!

Reduce Physical & Online Barriers

Reduce Physical & Online Barriers

IABG held its first biannual Coalition Connection meeting last month. These new coalition meetings provide opportunities to network with asset building practitioners and community leaders, learn about financial capability programs, and work together to advance policies that support the financial prosperity of Illinois families.

IABG held its first biannual Coalition Connection meeting last month. These new coalition meetings provide opportunities to network with asset building practitioners and community leaders, learn about financial capability programs, and work together to advance policies that support the financial prosperity of Illinois families. Our

Our